Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Public Affairs CSPAN December 6, 2012 10:00am-1:00pm EST

10:00 am

debt. sovereign entity states and governments, countries, will have debt to finance the things they cannot pay for out tried. i used to work an invisible bond department of a wall street firm. there were all kinds of bonds, which is debt of cities and countries and states. of course there is the federal debt. as i recall, some people with fiduciary responsibility are only allowed to select investments that have very high ratings. the highest raiders in the world, at one time -- rated in the world, at one time, was the

10:01 am

united states of america. and widows and orphans funds will invest in government bonds. host: alma, thank you for your call. we will consider your suggestion. the senate banking, housing and urban affairs committee is about to hold a hearing on the oversight of the fha program. shaun donovan will be testifying. we will be going to that as soon as that hearing begins. i want to show you this article in "the new york times took ." president obama plans to ask congress for about $50 billion for emergency funds to help

10:02 am

rebuild the state's the were ravaged by hurricane sandy. regional leaders complained wednesday it was not enough. the white house will send the proposal to capitol hill this week. it should be between $45,000,000,000.50 $5 billion, according to officials -- $45 billion and $55 billion, according to officials. both democratic and republican lawmakers from the region quickly expressed disappointment in the pending request and lobby the administration to increase it before sending it to congress. sue in oklahoma on our line for independents. i think we have time for your point. caller: in a column today it

10:03 am

said that clinton's 2001 balance the budget spent $1.94 trillion. today the revenue is $2.67 trillion. spending is $3.76 trillion. we are spending $987 billion more than if we had just increased the 2001 budget for inflation and population growth. i understand about the mores. i am incensed, as i think most voters are -- wars. i am incensed, as i think most voters are. host: the chair of the senate banking, housing and urban affairs committee is in his seat.

10:04 am

the ring with secretary donovan is about to begin. -- hearing with secretary donovan is about to begin. [captioning performed by national captioning institute] [captions copyright national cable satellite corp. 2012]

10:06 am

>> i call this hearing to order. thank you for joining us, mr. secretary. i asked you to testify today because i'm deeply concerned about the recent report that the f.h.a. could potentially need taxpayer support for the first time in its 78-year history.

10:07 am

i would like you to help the committee gain insight into the fiscal challenges at the f.h.a. and what h.u.d. has done and can do to mitigate losses and address the shortfall in the capital reserve ratio. f.h.a. has been helping save lives of the mortgage market by ensuring that qualified lower to moderate income and first time home buyers have access to credit since 1934. since the beginning of the financial crisis, the f.h.a. has increased its market share from below 5% in 2006 to about 30% at its peak volume in 2009, in pursuant of that mission. this cyclical expansion was essential to the mortgage market, especially for first time home buyers who have

10:08 am

comprised 78% of single family loans insured by f.h.a. in 2011. f.h.a.'s multifamily and health care insurance programs have also played an important cyclical role since the financial crisis with a fourfold increase in volume from 2008 to 2011. according to mark sandy, chief economist at moody's analytics, without the f.h.a.'s counter cyclical support, and i quote, the housing market would have quit taking the economy with it. providing the backstop for mortgage credit when public services flee from the market has a cost. the losses at f.h.a. to stem from the new now prohibited down

10:09 am

payment program, heavy losses in the first mortgage program, and losses -- loans made at the height of the crisis to prevent a collapse of the housing market. while they have already taken action to pretext the financial mortgage fund for single family loans from seeking federal funds, the f.y. 2012 report suggests that much more needs to be done to prevent such a draw. i want to hear more today about the administration's actions and proposals to minimize the risk to taxpayers stemming from their business and what safeguards are in place to ensure the quality and sustainability of the program. if the administration's actions and proposals will not be sufficient to restore f.h.a.'s

10:10 am

fiscal health, i'm inclined to work with my colleagues on both sides of the aisle on the banking committee to find a bipartisan way to make shoo -- that happen. before i turn to ranking member shelby, i want to recognize his work as ranking member on this committee over the past six years. this may be our last hearing together this year, and we will have no ranking member next year. i'm part of our bipartisan record over the last two years we continued it the tradition of bipartisanship that this committee has been known for by passing signature bills together this congress. and i thank senator shelby for his service. with that i turn to ranking member shelby. >> thank you, mr. chairman. first of all i appreciate your remarks. i have been on this committee 26 years, ending it, but i'm not

10:11 am

ending, i just have to move down a notch as i go over, hopefully, to be the ranking on appropriations. i won't be far away. i won't be far from secretary on h.u.d. stuff, either. but i enjoy working this committee. i enjoyed being chairman of this committee two congresses, the people on this committee are superb. the staffs are superb and this is a very important committee. not only for the senate, but for the american people and perhaps the world. as most people know, people are active on this committee because banking and housing and everything that goes with it goes right to the heart of what ticks in america. job creation, availability of money, the regulation of our banks, the securities and exchange commission t. money laundering, sanctions on iran, you name it. most of it, this is an active

10:12 am

committee, so i'll be around. right near here but i'll be yielding -- moving down one notch next to senator crapo, and will he do well. having said that, welcome again, mr. secretary. just days after the president's re-election, the f.h.a. released its 2012 actuarial report which revealed that the economic value of the f.h.a. fund has fallen to negative $16 billion. a lot of money. that means the fund's capital reserve ratio, as i understand it, now stands at a negative 1.44%. this news is obviously very disturbing to us and to the secretary. for those of us who have long been concerned about the health of the f.h.a. for years the problems of the federal housing administration have been well-known. during the housing boom, the f.h.a. unweissly, i thought, guaranteed -- unwisely, i

10:13 am

thought, guaranteed millions of risky mortgages with low down payments to borrowers with poor credit scores. we are reaping that now. these mortgages have resulted in billions of losses to the f.h.a. the federal housing administration has made matters worse, i think, by failing to come to grips with the magnitude, mr. secretary, of the problems. back in 2007, as the federal housing administration's poor financial position was becoming clear to all, including right here in this committee, i urged the f.h.a. to devise a credible plan to improve its finances. i stated then and i'll quote, that before the taxpayers are faced with greater loss, i believe we must determine how the f.h.a. got into this position, mr. secretary, and how it intends to get out. unfortunately for the past five years the f.h.a.'s leadership has understated their problems and sought to kick the can down

10:14 am

the road. this is now the fourth year in a row that the f.h.a. fund has been below its statutory minimum capital levels. yet each year we are told that this is a temporary dip and that within a few years everything will be fine. in fact, in 2009, mr. secretary, you told this committee that the drop in the capital ratio was expected to be, quote, temporary, and that it would, quote, return above 2% within the next two or three years, even if f.h.a. were to make no policy changes at all. we now know this forecast is way off the mark. the administration, however, continued to be optimistic. in 2011, for example, h.u.d. still had its projection showing the f.h.a.'s capital ratio reaching 2% in 2014.

10:15 am

now despite all these reassurances, the actuarial report projects that the f.h.a. fund has a capital reserve, as i meppingsed earlier, of a negative -- mentioned earlier, of a negative 1.44%. what is the response of the f.h.a.'s leadership here? just this year after further declines in the f.h.a. fund, both secretary donovan and acting f.h.a. commissioner carol gallant, testified to two different senate committees that the fund would, quote, return to the congressionally mandated capital reserve ratio of 2% by 2015. needless to say i'm not nearly as optimistic about the future of the f.h.a. i hope it works. i hope it does. the inability of f.h.a.'s leadership to clearly recognize and address its problems is raising doubts, mr. secretary, about the credibility and willingness to properly manage f.h.a.'s financing.

10:16 am

i think it's time for f.h.a. to face facts. we have to. first, the capital reserve ratio, the federal housing administration fund, is dangerously low. you know that. and has sha runge nearly every year since -- and has shrunk nearly every year since 2006. f.h.a.'s statutory obligations every year since 2008. third, every year since then future growth in the capital ratio has underperformed in relation to f.h.a.'s predictions. hopefully the shock produced by these latest projections will finally be a wake-up call for everyone. hard choices lie ahead for this program. we have talked about this. f.h.a. leadership, i believe, must fully realize its existing authority to shore up the value of this fund. additionally, congress must consider reductions in permissible risk layering and

10:17 am

further underwriting reforms and re-examine -- re-examination of premium structures. it's time, i believe, to get serious reform of f.h.a. before it needs a taxpayer bailout, if it isn't too late already. i wish you well, mr. secretary, but you have a real challenge here. we do with you. thank you. >> thank you, senator shelby. are there any other members who wish to make a brief opening statement? >> thanks, mr. chairman. just briefly i want to agree with the comments of our ranking member, mr. shelby. and our general concern is that we have seen this coming for a while. we have been talking about it. and the response from the administration has been very modest. unfortunately our worst fears are coming true, and even today i'm very concerned that the response even given this news is

10:18 am

just way too modest. in discussing last year's actuarial report, the acting commissioner, carol gallante, said there is no evidence or widespread prediction that home prices are going to decline to the kind of levels that would require a bailout. yet right now the question is quickly becoming not if but when. and still even in the testimony -- secretary's testimony today, we are only talking about things like waiting until the second quarter of next year to raise premiums and then it by 10 basis points. i really urge the secretary and others to consider other more aggressive, more proactive measures. mean "the washington post," which is not exactly a right wing think tank, said recently, quote, right now the critics are

10:19 am

starting to look pretty prescient. affordable possession of one's own home is the american dream. government support excessive borrowing has turned into a national nightmare, close quote. and the focus of that editorial was, we still haven't fundamentally reformed that, including at f.h.a. so i hope we start getting on that track starting today. thank you, mr. chairman. >> senator menendez. >> thank you very much. i'll be brief. i look forward to hearing the secretary's response on how f.h.a. balances the goals of remaining self-sufficient without taxpayer funds, but also helping what is still a fragile housing market in ensuring first-time home buyers can get credit. there is a clear case to be made in my mind that but for f.h.a. in the midst of this housing crisis, we would have a far

10:20 am

greater crisis on our hands. and so wreck siling -- reconciling the fiduciary responsibilities here to the taxpayers as well as the mission to people of america is incredibly important. i look forward to hearing that. and with your indulgence, mr. chairman, when it comes to my time in questions, while i certainly care about f.h.a., i have a even more pressing issue in the state of new jersey after thousands of homes were lost, lives were lost, and we are facing the greatest devastation the state has ever had. the secretary has been charged by the president in that regard, to be the, i call it, czar, but whatever the appropriate title is, and i will have some questions in that regard on behalf of my state. thank you. >> thank you. i want to remind my colleagues that the record will be opened for the next seven days for opening statements and any other materials you would like to

10:21 am

submit. now i would like to briefly introduced our witness, the honorable shaun donovan is the 15th secretary of housing and urban development. this is his ninth time before the full committee. secretary donovan, you may proceed with your testimony. >> mr. chairman. thank you, ranking member shelby, members of the committee, thank you for the opportunity to testify today regarding the status of the federal housing administration's mortgage insurance programs. i, too, want to add my thanks to ranking member shelby for his leadership and partnership on so many issues these last few years. this is an important moment for our housing market and our nation's economic recovery. as 2012 draws to a close, there are encouraging signs. housing construction growing faster than any time since 2008. the strongest year of home sales since the economic crisis began. and rising home values lifting 1.3 million families above water in the first half of the year

10:22 am

alone. f.h.a.'s programs have been a critical component of this recovery. that should come no surprise given the program's goals and history. with the dual mission of providing access for homeownership for underserved populations and critical financing for multifamily developments, nursing homes, assisted living properties, and hospitals, the f.h.a. is designed to fill gaps in the market, meet important commute needs, and act as a stabilizing force during economic distress. it's clear that f.h.a. has done just that. by ensuring much needed liquidity in the nation's mortgage finance markets, f.h.a. was a vital stabilizing force as we experienced the worst economic decline since the great depression. in the last four years, the f.h.a.'s made homeownership possible for over 3.5 million families, including 2.8 million first-time buyers, and for 50% of all african-american and latino home buyers last year. while f.h.a. has acted as a critical support, it has not been immune to the stresses of falling home values and rising

10:23 am

unemployment of the recession. according to the independent actuary's annual report on the m.m.i. fund, this fiscal year, the capital reserve ratio fell below zero to negative 1.44%, representing a value of negative $16.3 billion. we take and i take these findings extremely seriously. as stewards of taxpayer dollars, we have, since the start of this administration, made it a priority to strengthen the fund. and we are continuing to take aggressive action to return the fund to fiscal health, including those measures just announced in our annual report to congress. it's important for me to start by highlighting several key points that put the actuary's report in perspective. fully $70 billion in claims are attributable just to the 2007 to 2009 books and business. these three years are the major source of stress to the fund. in fact, in its report, the actuary attests to the high quality and significant profitablity of the books

10:24 am

insured since 2010, the strongest in the agency's history. it's important to understand this report does not in and of itself mean it will be necessary for the f.h.a. to use its authority to draw from the treasury to cover projected losses. while this possibility obviously exists, it is dependent on several factors. first, that determination would be made using the assumptions in the president's budget to be released in february, not the assumptions used in the actuary's report. second, we expect that the new books of business generated after 2012 will create approximately $11 billion in economic value, further strengthening the m.m.i. fund. third, since the actuarial report is a point in time snapshot, it does not take into account changes f.h.a. recently has announced to address the health of the fund. the final accounting of any shortfall would be done at the end of fiscal year 2013 in order to determine whether funds from the treasury are necessary. i'd also like to address the primary drivers of the decline

10:25 am

in the capital reserve ratio as compared to last year's projections. first, the house price appreciation estimates used by the ackture wary for this review were significantly lower than those used last year. that may seem counter intuitive given the economic progress we have seen, but the actual turn around in the market occurred later than was projected in last year's forecast. in addition, for technical reasons, the forecast is also somewhat artificially dampened by the significant increase in refinancing activity in the market this year. second, the continued decline in interest rates while good for the overall economy impacts the ackture wary's model by indcading marginally higher results -- indicating marnellally higher results. third, based on recommendations made by the g.a.o. and hud's i.g., and at the direction of f.h.a., in this year's report the actuary changed the way it reflects losses from defaulted loans and reverse mortgages in the economic value of the m.m.i.

10:26 am

fund. let me be clear, these are all important factors to consider when explaining the current status of the fund, but they do not minimize the seriousness of this report in any way. as i said at the outset, we have already taken significant actions to protect and strengthen the fund, including premium increases and changes to credit policy, such as increasing down payments for lower credit scarboroughers, and ending seller financed down payment assistance. with your help, our efforts have added well over $32 billion to the fund. the measures i will outline today further address the primary source of the problem. losses stemming from legacy books and business, particularly those insured during the 2007 to 2009 period and are designed to reduce our loss cevaerities by at least 5%, generating approximately $3 billion in economic value over the next two years. first, we have announced changes to our loss mitigation program that targets deeper levels of relief for struggling borrowers to more effectively assist families in meeting their

10:27 am

obligations and avoid costly foreclosures for f.h.a. similarly we are streamlining the use of short sales and aligning our practices recently announced to provide more families the opportunity to avoid foreclosure while reducing costs for the f.h.a. we have dramatically increased the use of alternative dispositions for defaulted loans, including our new distressed asset stabilization program. the improvement in recoveries from f.h.a. to this program is estimated over $1 billion this year alone. we are also taking proactive measures on new loans. in particular we are reversing a policy change made over a decade ago that allowed borrowers to stop paying premiums after their loans reached a certain loan to value ratio. this change left the f.h.a. without premiums to cover the losses on loans held beyond the period for which those premiums were collected. reversing the policy is expected to improve the val uste fund by $2.6 billion -- value of the fund by $2.6 billion in this fiscal year alone. in addition, we'll raise our annual mortgage insurance

10:28 am

premiums by 10 basis points. we estimate this will increase cost to new borrowers by about $13 per month, but it will also further reduce our footprint in the market while adding an estimated $1 billion of additional economic value to the fund this year. as private capital returns, f.h.a. must continue to balance pricing to ensure it occupies a smaller, healthier share of the market. in fact, f.h.a.'s market share has been declining since 2009 and 2012 represents our lowest volume year since the start of the economic crisis. while i focus today on f.h.a.'s single family programs, i wanted to take the opportunity to reassure the committee our efforts to protect our insurance funds span the range of our programs. we have already raised our mortgage insurance premiums on multifamily and health care loans, and instituted other risk management reforms such as special reviews for large loans, post commitment reviews by credit risk officers, and enacted loan -- an active loan committee process. even as we use our existing authority to take these measures to protect the fund, other

10:29 am

actions require your partnership. in addition to the increased indemnification authority and broader geographical enforcement powers recently passed by the house, we have a number of proposals designed to place f.h.a. in a stronger fiscal position over the next 12 months and beyond. including new loss mitigation authority, additional enforcement authority, and greater administrative flexibility in managing the reverse mortgage program. house has recently passed important bipartisan f.h.a. reform legislation and we look forward to continuing to work with both chambers to create the tools we need to strengthen the program, meet its mission, and place the m.m.i. fund back on firm footing. i encourage the senate to engage in discussions that build on this progress in the house in order to achieve a consensus that will give f.h.a. these tools as quickly as possible. there are no guarantees that the actions i have described will prevent f.h.a. from tapping into the treasury next september. however, swift action from congress, cuppled with the $11 billion in additional value from

10:30 am

the new fiscal year 2013 business, will reduce the likelihood that a treasury draw will be necessary. furthermore, these changes, as well as those we made over the past four years, have laid the foundation for a stronger f.h.a. and a healthier m.m.i. fund that supports the recovery of the housing market and economy, while actively reducing f.h.a.'s market share. as we work together to adapt and reform the f.h.a. program, we must proceed with a balanced approach that recognizes both the challenges to f.h.a. and its contributions to our economy. we are eager to work with you to achieve these shared goals. thank you again for the opportunity to testify today. i look forward to taking your questions. >> thank you for your testimony. as we begin questions, i will ask the clerk to put five minutes on the clock for each member. secretary donovan, i'm very concerned about the f.h.a.'s fiscal condition as detailed by the f.y. 2012 report, particularly the negative capital reserve ratio.

10:31 am

what action have you taken to restore f.h.a.'s capital reserve and prevent f.h.a. from requesting taxpayer support? >> mr. chairman, the most important actions that we have taken have been in partnership with this committee, and i would particularly recognize the fact that you passed a ban on seller funded down payments, which went into effect and we implemented in 2009. that action alone, we believe, has saved the f.h.a. fund about $12 billion. there are additional actions that we have taken. we have raised premiums four times. made underwriting changes that include raising down payments for the riskiest borrowers. that series of changes has added, we estimate, an additional $20 billion to the

10:32 am

value of the fund. quite simply, if we had not taken those actions in partnership with you, we would find ourselves in a vastly worse position today for the f.h.a. fund. >> mr. secretary, you have detailed several steps that would help stabilize f.h.a.'s finances. given the condition of the f.h.a.'s old books of business, why weren't these changes made earlier? will these changes allow the f.h.a. to outperform projections again this year and avoid drawing funds from the treasury? >> as i said in my testimony, i cannot guarantee that we won't need to draw at the end of the fiscal year. what i can say is that i believe we are taking all appropriate steps to try to avoid that. balancing both the health of the

10:33 am

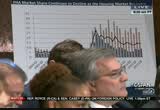

fund but also the fragile recovery that we have in the market. for example, we have already moved to increase premiums for the fifth time. we believe that that is an appropriate step and that it leaves f.h.a. appropriately priced. we would be concerned, however, about going significantly further in raising premiums, both because it would have potential negative impacts on the housing market. we are seeing a recovery, but it is still fragile, and we do not want to hurt the market and in turn hurt the f.h.a. fund by going too far to stop that recovery. but i would also suggest, as you see in the chart, on the right, we are currently, and the independent actuary confirms this, that the new books of business are highly profitable. and so i think there is beyond

10:34 am

the market question a question of how far do we go in visiting the sins of the past on new borrowers? the premiums being paid by new borrowers more than cover the expected losses. we think that's appropriately priced and will help to shrink our market share, but what we need to do is continue to focus on these older books of business and that's why i focused in the changes that we have made we announced in our report to congress on steps that will increase our collections from these older books of business. just from the asset sales that we have instituted and were going to ramp up going forward, we have increased the returns on these distressed loans by mortgage than 10%. simply with those steps. so we need to continue to focus on things and we have asked for authority from you to take steps that would help increase our returns on the older books of business. we think those are the most appropriate measures we can take. >> secretary donovan, one of

10:35 am

these steps is better loss bit myth gation by transferring insurancing from servicers who are underperforming. what is preventing f.h.a. from doing that under its existing servicing contracts? >> quite simply we need legislative authority to be able to force those transfers to happen. that is a critical step. it is something that we have seen in the private market start to increasingly happen. it's something we believe would be very helpful to send a very strong message to those servicers that are underperforming. but it is one of a number of a steps that we would ask that you give us legislative authority for as quickly as possible. >> one more question. secretary donovan, the act wearial report finding of --

10:36 am

actuarial report finding of the negative in the m.m. 1 fund is mainly problem legacy loans guaranteed during the housing bubble. what steps has f.h.a. taken to improve its underwriting dry teara and risk assessments -- criteria and risk assessments for the new loans? >> as i mentioned earlier, clearly the steps that you took to ban seller funded down payment loans were a critical piece of that. we also looked at the performance of our loans very carefully. so in addition to the premium increases, we did require a 10% down payment for our riskiest borrowers. that we believe was a very important step in changing our underwriting. we also have taken many other steps on other aspects of

10:37 am

underwriting that have to do with what costs can be rolled into the loan and other steps that reduce the effective risk of those loans that are quite important. part of that has been able to be done because, quite frankly, we didn't have a strong enough risk focus at f.h.a. in the midst of the crisis. we have created a very strong risk management focus through the creation of a chief risk officer for f.h.a. that's never existed before. as well as building a team of analysts that are really providing data on an ongoing basis on early payment defaults and a whole range of other information that we simply didn't have before in real time. so it's not only the underwriting changes themselves. it's also the focus on risk and the way that we are measuring it

10:38 am

on a real time basis that has given us new tools. >> senator shelby. >> thank you, mr. chairman. secretary donovan, lead me through this. tell me if i'm wrong on this or right or what. it's my understanding that under the statutes now prevailing that the federal housing administration could, if necessary, you deemed it necessary, tap the treasury for an endless supply of money. a lot of us would call that a bailout. do you anticipate that? can you assure us and the american people today as the secretary of h.u.d. that f.h.a. will not do that? or you don't know yet? >> senator, i wish i could -- hi a crystal ball and coy tell you that we won't at the end of the year. given the actuarial report this year, obviously i'm highly

10:39 am

concerned about that possibility. >> getting close? >> certainly we are closer than we have been in the past. >> how close are you? >> well -- >> honestly. >> what i will tell you, again, an independent actuarial report is the best can i give you in terms of that view. >> that's not good, is it? >> what it says -- >> the actuarial report is not good. >> it isn't. one important piece of this is that the -- what is required for the actuarial is a review as if we stopped doing business on the date of the actuarial. the important thing that we can do and that we have done to try to avoid taking funds from the treasury at the end of the year is to look at the revenue we expect this year, that's about $11 billion, and to make changes to underwriting and other steps

10:40 am

that would help avoid that. >> does that include up in the premium -- upping the premium a little? >> we have already moved to increase the premium an additional 10 basis points, an average of about $13 a month. >> how much money would that be projected? >> that would add about $1 billion just this year alone. and much more into the future. >> what is the size of your portfolio today, roughly? >> it is over $1 trillion when you combine -- >> $1 trillion worth of loans? >> when you combine all the various programs. >> how much -- how close are you as far as working capital so to speak? >> it's an important question. today, even though the actuarial report shows a negative balance, we have a cash balance of over $30 billion today. $30.5 billion. one of the things the actuary

10:41 am

looks at, assume we continue to do business, assume that we continue to operate, what is the likelihood, obviously we plan to continue to operate, what is the likelihood that we actually -- the cash balance goes negative? and the actuarial, despite the worst condition this year, still has a less than 5% chance that we actually run through all of those cash reserves. >> gives us the worst case scenario. it's the first week of december now. say three weeks, what's your worst case scenario, getting up to the first of the year, where you might be or not be? what would cause you to -- cause to you have a lot of heartburn say around the first of the year? >> the single greatest issue of concern is where the housing market will go from here. if the housing market continues to recover as it has this year,

10:42 am

that's the most important thing that we can see to restore the fund to health. house price appreciation is the single most important variable in the health of the fund going forward. it that is also why i will say we are so concerned about balancing the steps that we are taking to make sure we are not doing anything that would impede the recovery and come back and harm the f.h.a. in the long run by decreasing the improvement that we see in housing markets. >> we all realize that f.h.a. serves a good purpose, but it's just not sound financially. as the secretary of h.u.d., shouldn't the fiscal well-being of f.h.a. be one of your highest priorities? >> absolutely. absolutely. >> you're just going to deal with what comes up like you outlined today?

10:43 am

>> i would welcome additional ideas and suggestions that you may have. i certainly feel that we will take steps within our power. we would like to work with you, as i have said, as quickly as possible, to move additional authorities that would help us do this, but i am also opened today or any time to additional suggestions about what further steps we could take. >> if you do tap the treasury, in other words there's a bailout, so to speak, it's a sizable one, how would you pay that money back? premiums? better efficiency? the housing recovery? all of the above? >> we certainly believe that we need to keep f.h.a. in a position where our new books of business are producing substantial revenue for the taxpayer. this year alone we expect our new loans to return a $10

10:44 am

billion profit, if i could use that term, to the taxpayer. that is the way that we need to continue to restore the health of the fund and should we need to draw on the treasury to restore that money to the taxpayer. >> thanks, mr. chairman. >> senator reed. >> thank you very much, mr. chairman. thank you, mr. secretary. i repeat what my colleagues have said. it's very disturbing to have a report that shows 1.4% negative equity at a critical fund. and this is an issue that has not suddenly emerged. it's been brewing over several years. you have indicated that you are taking steps to fix these problems. and many people have said that in the past, too. again, can you sort of give us

10:45 am

some assurance that this time is different? >> what i can say, senator, is that i believe we are taking every responsible measure that we can to improve the health of the fund. while at the same time not hurting the fragile recovery that we have. i do not have a crystal ball and i believe that we need to continue to take input and guidance on getting a better picture of the fund. one of the reasons why the fund looks significantly worse this year than it did last year, we got criticism last year from outside experts, from the g.a.o., from our i.g. of the way that we model claims in our actuarial. we went back and directed our actuary to change the way we model, and that alone, that change alone, sub tracted $13

10:46 am

billion from the value -- subtracted $13 billion from the value of the fund. i'm not going to sit here and say we have been perfect in the way we looked at the fund or we have modeled it. one of my responsibilities is continue to make changes to get as accurate a picture as we possibly can and to take steps based on that. >> let me ask perhaps a related question, as you look forward in terms of the health of the fund, one fact would seem to me, i would assume it would be explicitly in the model, would be assuming about employment rates going forward. what unemployment rate are you assuming over the next year or so? because it directly affected payment -- >> absolutely. one of the important changes we made to the model this year not to get too wonky here, is to go to something called sacastic modeling.

10:47 am

we chose one path and modeled based on that. state of the art modeling, assigns probabilities to a whole different range of paths the economy might go through. we actually modeled a vast range of scenarios. one of the things we looked at last year that we directed our actuaries to look at last year was to say what if interest rates go low? what's going to happen to the fund? we ran that last year. that scenario predicted that the fund would go negative. in fact, we have had what is effectively the low interest rate scenario happen this year with qe-3. that was clearly had a substantial impact, roughly a $10 billion negative impact on the fund just from those interest rates alone. those are clearly steps that we are taking. we would be happy to share with you the various unemployment rate scenarios that we are looking at and home price paths we are looking at, but again we look at a range of those to get to the best possible prediction.

10:48 am

>> you got close to wonkiness with sacastic modeling. one of the problems that you face is this series of years of terribly mispriced loans in 2007, 2009. and it would seem to me one of the things that you are trying to do is to clear these as quickly as possible. but as you have indicated to us, you need help with servicing. that you have to do much more aggressive modification, sales, and also for the real estate that effectively alone, you have to dispose of it. can you comment on how much you think you can achieve in relieving pressure on the fund by doing that? looking back and taking care of that period? >> we think with a set of changes that we are already taking, that we announced in our report to congress with the actuarial, that include the loan

10:49 am

sales that we have taken, changes to short sales, changes to what we call our loss mitigation waterfall, how we work with borrowers that are in trouble, those alone could add about $3 billion to the fund over the next couple years. what we need help on is that many of our enforcement authorities, and again if you think about how we collect on the bad loans, enforcement is an important piece of that. to say to lenders, you made a bad loan, there was fraud or something else involved, we need to hold you accountable for that and bring funding back to the taxpayer. there are a number of provision that is would help us. one is giving us broader geographic authority. we have some perverse restrictions right now in legislation in terms of the way that we can hold lenders accountable on a narrow geographic basis. what we can do to require indemnification of loans, the

10:50 am

standard for fraud, those are all pieces of what we would want to work with you to get past very quickly -- passed very quickly to enhance our enforcement authority. those as well would likely add billions of dollars to the fund. as you know we have been able to recovery well over $1 billion just this year in settlements around servicing and originations with many of our biggest lenders. >> thank you very much, mr. sefpblgt thank you, mr. chairman. >> -- mr. secretary. thank you, mr. chairman. >> thank you for your testimony today. you asked for some suggestions and i'd like to make just a few. it's my understanding that on the private side right now fico score is really at 620, where the market is. and f.h.a. is at 580 and basically it's creating a situation where the private lenders are being made out to be bad guys because even though

10:51 am

your fico scores are 580, they are not doing anything before -- below 620. as one of the steps that you might take, would it make sense for you to go ahead and get on up to 620? right now there's huge demand out there, and at some point that's going to diminish and will drive back down as people try to get market share again. would it not make sense to go ahead and implement what the market is telling you to do? >> that is something that we are actually looking at. i think it's likely that we take additional steps as we are working towards the president's budget and understanding in more detail the results of the actuarial. that is clearly something we are looking at. we are concerned that some of the overlays that lenders are putting on go farther than are necessary. in other words, we do believe that there's been an overdirection, if you will, in

10:52 am

some parts of the market, where we have what are very safe borrowers that are having a hard time accessing credit. but i also agree that we need to be looking at and perhaps adjusting on the fico side as well. >> generally for what it's worth, i appreciate your testimony today. i know we have had discussions about that sometimes in the past. and i do realize you had a lot of bad loans on the books that you inherited. i do think there are things you can do now to really cause the fund to be more -- far more sound. i do think you all are being slow in moving that way. a second one i would move to is reverse mortgages. you are losing your shirt on reverse mortgages. losing your shirt. it's a small part of what you're doing, and yet you've got mortgage brokers out there that are making an absolute fortune right now, a fortune. some of them are good operators. a lot of them are sloppy operators. i don't understand why you don't shut the program down for 24 months as i know has been suggested to you?

10:53 am

why don't you do that? >> once again, senator, you have hit on an issue that is an important one and that we do believe we need to make changes. >> why don't you just do it? >> frankly, we did make changes. we introduced a much safer, better, we thought, alternative through our safer -- saver program. we could effectively do what you said, which is to just create a moratorium on the other program. what we are concerned about is particularly given the economic crisis that seniors have gone through, that we would be eliminating an option that works for some seniors, if it's done safely, in order to eliminate also the bad loans being made. our preference, if we could get authority from you to change the structure of the program to make it much more effective and safe, that would be a better way to go. if we can't get that authority

10:54 am

quickly, we'll have -- >> i would think -- why can't we do a unanimous consent, it seems to me most people would be willing to do that? >> let's talk about that today. i would love to -- >> i know you've got a partial situation that has been very healthy. it seems to me if you're worried about seniors, you could keep the ability to draw down a partial amount which is very safe, and you would eliminate -- you could do that all by yourself. and we could worry about the legislation whenever it's time. i'm willing to look at it now. just for what it's worth it does feel like there's a lot you could do to make f.h.a. healthy today that is not being done. let's talk further, ok. loan limits. seems like right now, fannie and freddie are down at 625. are you still up at 729. wouldn't it make sense to go ahead now and make some changes that need to be made? you can do that yourself. why don't we do that?

10:55 am

>> as i think you know, we supported our loan limits coming down. and they were supposed to expire last year. congress made the decision to allow -- lower the g.s.e.'s loan limits but kept f.h.a.'s -- >> can you self-implement that? you cannot do that? >> i do not believe that given that congress explicitly extended those higher limits, that we can take that step. >> would you like for us to help you do that? >> we have supported before and i will state again today that going back to the limits makes real sense. i will go further than that, that we should lay out a path to go back to even lower limits that existed before the crisis in a way that is done consistent with how we do housing finance reform. that is is larger question. but the immediate step of going

10:56 am

back to the pre-era limits is one we would support. >> are you developing a fan. and i hope we could look at some of those things. home mortgage insurance. the way i understand that it works is private mortgage insurers when you get down to a certain loan to value ratio, the insurance -- the premium is dropped, but also the insurance is dropped. and yet you have a trillion dollars in loans on your books where the loan to value has dropped. they are no longer paying premiums, but you are keeping the guarantee in place. that doesn't make any sense to me. and why don't you continue to make the homeowner, who has that guarantee, continue to make the premium payments? that would be something that seems to me would be extremely helpful to you during this difficult time. >> once again, an excellent suggestion. we announced with our report to

10:57 am

congress that we were -- we are doing that for new loans. >> why not the ones on the books? >> unfortunately we can't go back and modify a contract. when that homeowner took that loan, they signed a deal with f.h.a. that said this is the way the premium structure would work. we looked at this. we fully analyzed it. we can't break those contracts, unfortunately. and so it's something that we are going to need to implement. i will say, however, that the value of doing it now in a low interest rate environment is substantially larger on these new loans for two reasons. the lower the interest rate, the faster the am more at thisization of the principal and therefore this will be a more valuable change. second because these loans are so low interest rate, they will be on our books far larger. frankly, not many loans in the past have hit that limit. so even though it's $1 trillion portfolio, the value of that change is quite small for the old loans. it's really going to be quite

10:58 am

valuable for these newer very low interest rate loans. >> i'll be briefly two more questions. i see that f.h.a. is now making loans to people who three years ago were foreclosed upon. and that's a very different standard than even exists at fannie and freddie. i don't understand. why are you doing that? >> this is another area where we are working on changes. here's the issue. we have a significant number of homeowners that were responsible homeowners, had good credit scores that lost their jobs in the biggest economic crisis this country has faced since the depression. and we believe if somebody can show that they are back at the work and responsible borrower again, that that's somebody that we ought to work with. i would agree that our standards

10:59 am

are not clear enough in dividing those. so what we believe we need to do is clarify those standards but not necessarily eliminate the possibility that somebody who has done the right thing and through no fault of their own lost a job but can be a responsible homeowner again, has the chance. my view would be it's not just the three-year limit that's important, it's what are the criteria that we set for how somebody re-establishes their credit and being a responsible homeowner? >> my last question, thank you for your patience. first of all it sounds like there is a lot of things -- there are a lot of things that could be done right now to solve a lot of problems. and i hope that we as a committee will figure out a way to work with you on those things. we need to work with you. but you can do the things you can do now. you and i had a pretty long conversation several months ago when carol gallante had the opportunity, candidly, to assume her post on a permanent basis.

11:00 am

and we could not get the administration to agree to not airdrop something and bypass the committee. it's an unfortunate circumstance. but i guess as i look at it, i would just ask you the question, did we dodge a bullet in appointing her full-time with all the issues that we have at f.h.a.? and does she really have the ability to press the administration to overcome political issues to actually cause the fund itself to be ack actuarially sound? because it appears to me that we are still not quite doing the things we ought to do to make the fund operate. it seems to me maybe there's a little political pressure and maybe she's not strong enough to make thatp. . >> we have taken the most aggressive steps i think in the history of the agency to make sure the new business that

11:01 am

we're doing is strong. if you look at that chart right there, what you'll see is huge profitability relative to the history for the new loans that we're making. we have only so much that we can do to fix the problems of those older loans. so i agree with you on many of the steps that you described today. what we shouldn't imagine is that somehow taking those steps can take us from the difficult financial condition that the f.h.a. finds itself in today, somehow to eliminating what has been an enormous trauma in the housing market. i have enormous confidence that carol can and will lead us to that -- on the path that we need to take and in fact you don't have to take my word for it. i think the evidence of the changes that we have made, the steps that we took, you remember last year the

11:02 am

president's budget thought that we might need a draw at the end of last year. carol took aggressive steps on enforcement, on changes to underwriting, that meant instead of a negative close to a billion-dollar balance, we ended the year with a more than $3 billion positive balance. those were aggressive steps that she took. i listened to her but she took those. and i believe that that's the kind of leadership that can help us continue down this path. >> thank you. senator hagen. >> thank you, mr. chairman. and, mr. secretary, thanks for your testimony today. i know that senator corker asked about reverse mortgages. and i am concerned about that issue and i'm particularly concerned that $2.8 billion of the $16 billion economic shortfall are related to that program. can you talk a little bit more about why these losses under the reverse mortgage program are so is he rear?

11:03 am

>> here's the fundamental problem. without getting into too much of the history. at one point when fannie mae was issuing these loans, they were generally variable rate and they could -- they allowed a borrower to basically draw on a, you know, over time, the amount of money that they needed. as that program has switched to being a ginny may program, there is basically no option for those borrowers to do anything but draw the full amount. >> and why? >> because we don't have the statutory authority to be able to make the changes to the program that would allow us to limit the draw up front. that's the change that we're asking that be made. our alternative, and i was just discussing this with senator corker, we could basically eliminate or put a moratorium on our regular program and just go to what we call our saver

11:04 am

program which is somewhat safer. but the problem is, we still don't have the authority even under that program to avoid this full draw feature of it. and -- so the right answer in our view is, give us the authority to make the changes we need so that we end up with what is a safer product for s.h.a. and frankly a safer and better product for seniors. what we're finding is with this full draw product too many seniors end up in situations where they can't cover their insurance and their taxes and too often we lead to a situation where they have more leverage, more debt, than their home is worth by the time they're ready to sell that home. >> so you're saying because of that change, that's what resulted in the huge $2.9 billion. >> that is for many of these -- for most of the new loans that we're making, they're at this full draw and they -- the actuary predicts they're going to be enormous losses on those

11:05 am

going forward because of this full draw feature. >> ok. and also, the last time you testified before the committee, we discussed the national mortgage settlement. can you talk briefly about the m.m.i. fund, how it's benefited from the settlement? >> in the most direct way it's benefited by well over $1 billion that came directly to the fund from that settlement. or that series of settlements. also important, though, is we put in place not just for fmplet h.a. loans but for -- f.h.a. loans but for every kind of loan that were serviced by the banks that were part of it, new standards for how they foreclosure on loans, how they work with troubled borrowers and in the long run those

11:06 am

changes will have very important affect not just for homeowners and communities but also benefits to the f.h.a. fund because we will have fewer foreclosures and better recoveries on the loans, whether it's in short sales or keeping home owners in their homes. >> the settlement also includes billions of dollars in debt forgiveness for the borrowers and generally discharge of indebtedness is taxable to borrowers but certain exceptions exist for indebtedness related to principle residencies. this is set to expire at the end of this year. what's the interplay of the expiring tax provision and principle reduction for borrowers and how would the expiration of that provision impact participation in the settlement and the relief that borrowers -- >> it would be a cruel irony if homeowners have the ability to stay in their homes because of a principle re-- principal reduction that is both good for

11:07 am

them and their lender because it's going to lower the losses on that loan in the long-term. only to get, come tax time, a giant tax bill for that principal reduction which drives them back into the delinquency and potentially foreclosure. and so the president has made it a real priority to try to get that provision into the tax -- whatever tax extenders we may do at the end of this year. and it is a very high priority for us among the many things that will be at issue in that tax extender. >> thank you, mr. chairman. >> senator. >> thank you, mr. chairman. thank you, mr. secretary. again, as i said at the beginning, i have the real concern that i think is shared by a lot of committee members. that the changes in reform, f.h.a., has made, you're

11:08 am

talking about today, aren't significant enough given the looming threat. and you say they're unprecedented. that could -- both of those things could still be true. they could be more than ever before and still not enough given the magnitude of what we're talking about. and that's the concern. first of all, let's talk about the clear potential now for a taxpayer bailout. is it not right that under the federal credit reform act it would allow the treasury to make necessary cash or credit transfers to f.h.a. in order for them to continue making payments sort of automatically? >> that's absolutely correct. that is the way not only f.h.a. but other similar programs are designed. >> that's obviously significant for the taxpayer. we all care about that. can you commit to us that you'll keep us and the congress fully apprised of your moving

11:09 am

projections with regard to that and certainly fully apprised when that happens? >> i'm absolutely committed to make sure that if we're going to take that step, that you would be fully notified. >> my question was a little more than that. it was to keep us fully apprised of your current and updated projections toward that issue. can you commit to us to give us that information, your best projections, today and whenever that changes and certainly if that's going to happen? >> i do and, senator, what i would suggest, we do provide a monthly report to congress on the status of the fund. if there's additional information or somewhat different information that would be useful to you in that, we are very happy to work with you on that. >> ok. well, what i'm talking about is as of today, when do you project that's going to have to be a taxpayer-funded bailout? what's your best projection?

11:10 am

>> what i would say is our best projection will be contained in the president's budget. we are still working on the underlying economic assumptions that go into that. and so i don't have anything beyond what the actuary did that would be a different prediction to that. >> so today with an all of h.u.d. and all of f.h.a. you have no best guess about that? >> i'm not sure what you would suggest is a best guess other than to say the actuaryial report has a value of the fund as of the date it was performed, in addition to that we expect about $11 billion of new revenue and the changes that we've implemented we believe will bring billions of dollars of additional revenue to the -- >> based on all of that, do you expect a taxpayer bailout as we

11:11 am

sit here today? if so when? >> based on those steps, i believe we have significantly decreased the chance of having a bailout at the end of 2013 or having to draw on the treasury. i'm not going to assign a probability at this point because we are still working on the assumptions and other steps in the budget and i will be able to give you a number when we've completed the budget projection. >> again, i want to reask for your best information about that as it develops. and unfortunately we don't have that today. i think y'all have some idea, some best guess, you're not giving it to us. we'd really like that as soon as you can give it to us and from then on, on an updated basis. with regard to changes that are being made, you just said they're unprecedented and the proof is in the pudding and the changes that were meat in the last year -- made in the last

11:12 am

year stepped us back from that possibility. i just want to add for the record, there was another big factor, $1 billion in the a.g. settlement. that was underfound money. it was a huge factor that had nothing to do with reforms or changes. but i also want to associate myself with senator corker's suggestions about a whole menu of things that we believe exist that y'all are not doing that i believe is warranted. there's several ways, and senator corker touched on this, that f.h.a. has much laxer standards than fannie mae and freddie mac. and as a result are you creating a huge magnet to draw the worst problem loans to f.h.a. because of that. one of those is maximum loan limit and another is the issue he brought up of allowing a borrower to reborrow three years after a foreclosure. fannie mae and freddie mac, that's four to seven years. on those two things and anything else like that, why

11:13 am

wouldn't you align f.h.a. with fannie mae and freddie mac to stop this negative selection that is occurring toward f.h.a.? >> senator, two things i would just say. one is, it's not accurate to say that the reason the fund remained positive last year was because of the settlement. the value at the end of the year was over $3 billion. if the settlement had hadn't happened we still would have been positive and the second thing i would say with is i don't see the settlement as unrelated to policy changes. strong enforcement is particulate of what we need to do -- part what have we need to do to make sure that we hold lenders accountable and that we minimize losses from those older books of business which are causing the stress to the fund. and so i believe very strongly it was the right policy decision. it is related to steps that we've taken. and even if it hadn't happened, we would have remained positive last year.

11:14 am

so, on loan limits, as i said before, we do not have the authority without congress acting. the administration advocated that loan limits come down. i thought it was frankly perverse to keep fannie mae and freddie mac's -- to bring fannie mae and freddie mac's loan limits down and not to lower f.h.a.'s at the same time. exactly for the reasons that you've said. we are concerned that it would drive business to f.h.a., that should go back to the private market. so i would urge you and others, i know you're supportive, but to work with your colleagues to try to do that as quickly as possible. and i do agree that we need to look at and we are doing that, looking at the standards for how we allow borrowers who may have defaulted in the past to borrow. again, i would say, though, we should not hold a responsible homeowner who has demonstrated their ability to pay back their debts and to be a homeowner, a

11:15 am

successful homeowner, simply because they may have lost a job due to what is an unprecedented economic crisis that we've been through. so this is not just about time lines. it's about what the standards are for when we allow folks to borrow. >> well, my broader point is this and several other factors should also be about doing it in a way that you're aware of what competing opportunities rules are, like fannie mae and freddie mac. and if f.h.a. has laxer standards, i mean, clearly you're going to encourage the accumulation of weaker loans. i think that's obvious. >> yeah, i agree with you. one of the things that we announced just a few weeks ago with the act warle report is that -- act wearial report is that we are implementing standards on short sales which are aligned with what fannie mae and freddie mac are doing. so we are looking for opportunities wherever we can to try to align those standards. that doesn't mean on everything that we should be identical to

11:16 am

them. >> another significant factor in terms of potential loss is the whole reverse mortgage program. which is projected to be a drain on the system, even in the best economic circumstances. and as i understand it, f.h.a. has the authority to suspend that program. it's a huge profit center for folks who participate in the private sector. it's costing the taxpayer money essentially. or threatening exposure in the best of times. why wouldn't we suspend that tomorrow? >> that is an option that we are clearly looking at. we believe there is a better option which will be to get legislative reform to allow us to implement a better product.

11:17 am

that is something, as i talked about with senator corker, we'd love to work with you on the next few weeks. the house has passed an f.h.a. reform bill. we'd love to be able to do something even in this session of congress before the ranking member -- >> let me -- >> senator vitter, please can you wrap it up? >> sure, i'll wrap it up very quickly. let me suggest melding those two ideas together. i think if you suspend that program tomorrow you'll start saving the taxpayer money and create more pressure for the reform you're describing. thank you. >> senator men endezz. >> thank you, mr. chairman. mr. secretary, while i clearly have question ises -- questions about san joaquin, let me just create some balance -- sandy, let me just create some balance here for my perspective. first of all, am i wrong to say that the h.u.d. report says

11:18 am

that f.h.a. continues to be impacted by losses from mortgages originated prior to 2009? >> that's exactly right. and, senator, if you look at the chart on the right here, what you see is that through 2007 and 2008 in particular, we have huge cost to the fund. that 2009 we saw still negative impact but real improvement and then in 2010 through twelve those loans are expected to contribute substantial revenues to the fund and to the taxpayer. >> so a good part of the portfolio that we've been suffering with here certainly took place prior to this administration? >> that's correct. but i would also give you all credit for acting to end the down payment at the end of 2008 which we implemented in 2009. >> now, i know there was some talk about the higher loan limits in your own view but let

11:19 am

me just say, doesn't the audit also say that, quote, larger loans tend to perform better compared with smaller loans in the same geographical area? >> our early data is that these larger loans are performing somewhat better. we do believe, however, it's too early to make any final conclusions about it simply because these loans haven't had much time to season at this point. >> it seems to me that so far they have probably strengthened f.h.a.'s balance sheet by allowing larger, better performing loans. and there's a problem here. there's parts of the country in which those lower loan limits would make f.h.a. virtually not as valuable to its core mission as it would in other parts of the country which is why on a bipartisan basis we passed, preserving the higher loan limits. so i'm looking forward to

11:20 am

seeing the continuing performance of them. because i think it would make another case. and i'm waiting for the private sector to come in. i mean, i keep hearing about the private sector ready to come in but it just doesn't seem to be happening. now, there are some who would suggest that mrs. gallante hasn't been performing well, maybe my eye sight is not good but i look at that second chart and it seems to me in the time period that she has become the acting head, that in fact the performance of the portfolio under her watch has gone from the negative performance that existed before her watch to a positive performance significantly during her watch. is that a fair statement? >> it's absolutely fair. i would add the chart just to the left of it also shows that we've done that while reducing f.h.a.'s market share. so we have taken steps to try to bring private capital back, to string our market share. but still to have the

11:21 am

performance improve substantially. >> do you have a different view than moody's data that shows that the f.h.a.'s presence in the market prevented housing prices from dropping another 25%? >> i think that's as good an analysis, as thorough an analysis, as we've seen of the important impact that f.h.a. had on the market and frankly what would have happened if we had not been there, as you see. congress intended f.h.a. to be here when the country went through a crisis. either a regional crisis where there wasn't lending available, or a national crisis. and that's exactly the role that f.h.a. played with that increase in market share. we agree it is time, as the market is improving, to shrink that share. but not to do it in so precipitous a way to raise premiums or to take other steps that would hurt what is still a fragile recovery. >> i would simply say that in a time in which the housing market, although we see some

11:22 am

indicators moving upward and prices, values moving upward, that it's still a very significant challenge. and just like a doctor, i mean, i think the principal starts -- principle starts off with you do no harm. especially when you're in the midst of a challenging recovery. so i look forward to seeing how we move in this dual track of making sure the taxpayer are held whole but at the same time preserving some of the core missions of f.h.a. i want to turn to hurricane recovery. this hurricane, mr. chairman, we're not used to hurricanes in the northeast. we have been blessed not to have them. but when you have a superstorm that comes with full moon, high tides, and a drawing in of what was a hurricane because of a front that came from the west, you have a perfect storm in all

11:23 am

of its iterations. i've lived in the state of new jersey my whole life. i have never seen the type of devastation that exists in the state. the pictures that some of my colleagues have seen on television and whatnot do not do justice to the depth and scope of devastation. we have thousands of people who don't have a home to go back to. i know that when people talk about the new jersey shore, because of some of these shows, they think of a certain thing. these are people's homes. i'm not talking about second homings. i'm talking about their lifetime homes. year-round communities. that don't have a home to go back to. i'm talking about a $35 billion tourism industry that is largely devastated. i'm talking about the megaport of the east coast, the port of new york and new jersey that suffered huge damages, $250 -- 250,000 jobs, $30 billion of economic activity for the nation, national security because we closed the only port

11:24 am

in the northeast that was a military port and now we use the commercial port for forward deployment when we need to. in the case of emergencies. you know, and i could go on and on. so, mr. secretary, in your other role here, i want to get a sense from you as to the commitment of this administration and the federal government to helping new jersey, but certainly new york as well, and the region recover. because when we had hurricane katrina in the gulf coast in mississippi and alabama and louisiana, i was there. when we had tornadoes in joplin, missouri, i was there. when we had flooding along the mississippi, i was there. when we've had crop destructions in the midwest, i've been there.

11:25 am

because i believe this is the united states of america. so i fully expect that now that for the first time we have the type of devastation that others have suffered and should understand, that we're going to have the type of response that others have received. and so i'd like to get a sense here, i know we're working toward this goal, but i'd like to get a sense from you as to the type of commitment that this administration has toward those goals. >> senator, thank you for the eloquent remarks about this. as you know, this is a region i too have deep roots in. i think to use your term, i married up, i married a jersey girl. and have worked in new jersey, grew up in new york. besides the personal commitment i feel, i've also seen a president who was on the ground in new jersey almost immediately, has done

11:26 am

everything he can to help the short-term and has given me the responsibility to help make sure that this recovery is a full, complete recovery. not just to build back what was there, to build back smarter and stronger. so you have my commitment that we will do that. we will propose a supplemental this week that i hope you will see demonstrates that commitment. but we will also be committed to making sure that we get that supplemental passed in the next few weeks because, frankly, there are too many homeowners, too many small businesses, too many renters that have the lives that are simply on hold until they know what resources will be available to them to rebuild. fema cannot by statute provide for a full recovery. they are a response organization. and we need to take further

11:27 am

steps through a supplemental this month to be able to move toward a fuller recovery and give those families, those businesses, some hope that there is a future for them in new jersey and around the region. >> mr. chairman, let me close if i may with your indulgence because of the nature of this issue by saying, number one, we await what the supplemental looks like. and we'll reserve judgment until then. number two, we need -- regardless of the size of the supplemental, we need flexibility in being able to seek the recovery that we all want. number three, in addition to a per ferm storm, there's another perfect storm here. we get this storm in the midst of the beginning of winter. and most of the hurricanes are in gulf seasons, in summer seasons, totally different in terms of the consequences to people, huge in terms of the impact but still time to recover without the rave ashing of the -- ravaging of the winter months. if we have a nor'easter our

11:28 am

defenses are so far down that would be like a person's immune system being susceptible to any type of illness. and thirdly, we come with less than 30 days to the end of the congress. in which this has to be done. i feel like i have to be hue dinny to accomplish this -- hue deany to accomplish this -- hue dinny to accomplish this. but we're going to do this. we're going to do this. secretary, i look forward to your work and your help as we get there and to our colleagues as well. thank you, mr. chairman, for your indulgence. >> i would note that senator men endezz will chair -- menendez will chair a hearing next month, december 10, on superstorm sandy. >> thank you for joining us. i would like to understand better an aspect of the act warle review. -- act warle review.

11:29 am

-- act wearl review. -- actuarial review. you observe on page eight of your testimony the fact that the lower the interest rate environment the worse shape the fund is to simplify things. you walk through the mechanisms by which lower interest rates, while good for the economy overall, tend to have an adverse impact on the value of the fund. my understanding is that the actuarial review contemplates a low interest rate environment. and in the low interest rate environment the value of the fund is negative $31 billion. are we in a low interest rate

11:30 am

environment today? and aren't we by virtue of what the fed has said, which is to say maintaining current policy at least through mid 2015, so three years or so, at least, isn't it very likely we're going stay in the low interest rate environment and shouldn't that be the prevailing environment assumption? >> you make a very important point in terms of the fact that the actuarial review was done not today but at a point with economic projections that are primarily in july over the summer. and so it's accurate that interest rates have dropped further than were built into the primary actuarial view. there are two offsetting factors to that, though. one is that home prices have performed better than were used

11:31 am

in the actuarial. and that, based on what we know today, even for this year the actuarial would be significantly better if it were performed today just on that one variable. and then the second point is that the act warblee review is a -- actuarial review is a point in time that assumes that we do no further n.h.a. business. an one of the things that's article about it if i can use that term is that when interest rates go lower, it assumes people pay off faster. that's accurate. what it doesn't take into account is that typically about half of those folks refinance into an f.h.a. loan. so, by the nature of the actuarial, taking a snapshot in time, assuming you're closing down the fund, there are revenues that will come to the fund that aren't built in. all that being said, we will in the president's budget include

11:32 am

the lower interest rates that you describe. we will also include an updated projection of house prices and at that point will have a clearer picture of how these offsetting factors play. but it wouldn't be accurate to say that the right number is today, the $30 billion or $31 billion. >> do you believe that the difference in home prices that prevail today versus at the time that this was done, and the difference in the volume that you refer would be enough to offset the lower value that is caused by the fact that we are in a lower interest rate environment? >> the truth is just to be honest, we haven't fin hished those calculations. we're in the midst of doing that for the budget. what we will tell you is they are both large effects and it is certainly conceivable that they could be offsetting or in the rage of offsetting. but we simply don't have an answer to that. >> it's a pretty large effect

11:33 am

that comes from the difference in the interest rate. do you know what the lower interest rate environment scenario assumes for the 10-year treasury yield by any chance? >> let me ask my crack team behind me to get that. we'll have that for new a moment. >> all right. i mean, my guess is, i'm not sure a team, even that assumption, is as low as the rate is today with an interest rate, a 10-year treasury of about $1.6 -- 1.6%, it's shockingly low. we have a fed insisting it's going to keep it this way for a long time. so i'll be very interested in seeing what the net effect of these changes are. we know the interest rate component is -- will reflect a significant adverse valuation here. >> yeah. but again, i would just point out that there is an artificialality of the point in time because it doesn't -- it presumes every one of the payoffs we have no more revenue to f.h.a., whereas in fact we know a large number of those re financing -- >> so you're saying there's a flaw in the model for that.

11:34 am

>> no. congress requires that the actuarial review be done in a way that is a -- what we call a runoff scenario. we also in the actuarial look at what if we keep doing business, so we have those projections in the actuarial. that's not the 2% calculation but it is something that we could give you more detail on from the actuarial of what the net effect would be with the refinances. >> does the modeling assume any recession between now and 2017? >> the model thing does include a range of runs from a mild recession to a very severe recession and through the kind of nature of the modeling we do look at probabilities for those recessions. >> but does the valuation, the model that comes up with the valuation of negative $13.5

11:35 am

billion, does that assume a recession? >> it looks at -- it assigns probabilities to the potential for different types of recessions and builds those in. i'm not sure if i'm being clear. but it is not -- >> what is the average economic growth rate that's implicit or explicit in that valuation? >> again, i can get that for you momentarily. >> ok. my last point, the senator from new jersey made a very important and impassioned argument about the feablingts of hurricane sandy. in pennsylvania we had very significant damage but exclusively from wind. almost entirely from wind damage. millions lost power. but the damage wasn't comparable to the damage that was compounded by the water damage, of course, that was done along the shore. i'm looking forward to seeing a supplemental that is well crafted and i hope properly offset. because we also have a fiscal crisis of enormous magnitude.

11:36 am